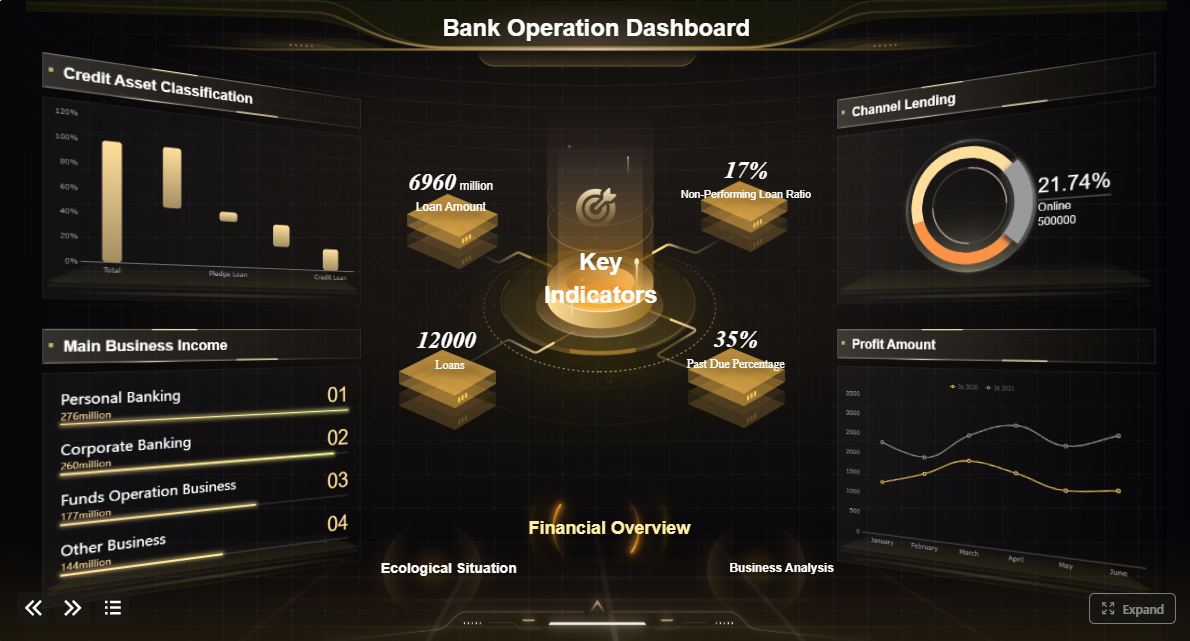

A banking dashboard is a decision system that consolidates financial, customer, risk, compliance, and operational data into one interactive view. For banking leaders, that matters because critical decisions cannot wait for disconnected spreadsheets, delayed monthly packs, or static reports that hide root causes.

If you are a branch manager, operations director, risk lead, or executive, the pain points are familiar: fragmented systems, inconsistent KPI definitions, slow reporting cycles, weak visibility across channels, and too much time spent reconciling numbers instead of acting on them. A well-designed banking dashboard solves this by turning raw banking data into a role-based command center for performance, control, and accountability.

Click To Try The Dashboard

Click To Try The Dashboard

A banking dashboard is an interactive reporting interface that brings together data from core banking systems, loan platforms, CRM tools, digital channels, treasury systems, call centers, and compliance workflows into a single decision view.

In practical terms, it helps a bank answer questions like:

Unlike a static report, a banking dashboard is built for action. It offers:

This is why the same banking dashboard framework can serve multiple users across the institution:

The business value is straightforward: faster decisions, earlier interventions, stronger governance, and better performance management across the bank.

A banking dashboard is only as useful as the KPIs it surfaces. Too many dashboards become cluttered because they display every available metric rather than the few that drive decisions. The goal is not more charts. The goal is sharper management action.

Financial KPIs help banks assess growth quality, margin strength, and product economics.

Key Metrics (KPIs):

These metrics give finance leaders and executives a top-line and margin view, but they also help department heads understand where profitability pressure is coming from.

Modern banks cannot evaluate performance through branch activity alone. Customer behavior now spans branch, mobile, web, ATM, call center, and relationship channels.

Key Metrics (KPIs):

These KPIs help banks balance growth with experience, while also showing whether channel migration strategies are delivering value.

Risk visibility is one of the most important reasons banks invest in dashboarding. Senior leaders need early warning signals, not retrospective commentary.

Key Metrics (KPIs):

A good banking dashboard does not just show these risk metrics. It connects them to business units, portfolios, and workflow owners so action can be assigned quickly.

Operations dashboards help banking teams improve service speed, control work volumes, and reduce avoidable cost.

Key Metrics (KPIs):

These metrics are especially valuable for operations directors who need to move from anecdotal bottlenecks to measurable process control.

One of the biggest mistakes in dashboard design is assuming one dashboard can serve everyone equally. In banking, decisions happen at different layers, and each layer needs different granularity, timing, and context.

The three main decision-making layers are:

Executive banking dashboards are built for strategic oversight. They should focus on trends, exceptions, and target attainment rather than operational clutter.

A useful executive dashboard typically includes:

For executives, the dashboard must answer one core question: Where does leadership need to intervene now?

That means concise visual design, clear target tracking, and drill-down capability when a number moves outside tolerance.

Management dashboards sit in the tactical layer. These are used by heads of retail banking, lending, operations, contact center, treasury, collections, or regional management.

Their role is to translate strategy into supervised execution. Typical use cases include:

These dashboards need more context than executive views. Managers need to move quickly from trend to cause, and from cause to accountable owner.

Operational and analyst dashboards support day-to-day banking execution. They are the most detailed and often the most actively used.

Common features include:

For analysts, drill-down and filtering are essential. They need to isolate trends by time period, branch, portfolio, risk band, or journey step. For frontline teams, the dashboard should reduce friction and help prioritize the next action.

The value of a banking dashboard becomes clearer when tied to real scenarios. Different banking functions require different dashboard designs, but all share the same goal: turn fragmented activity into coordinated decisions.

Retail and branch leaders need visibility across network performance, customer activity, and service quality.

Common dashboard use cases include:

A branch performance dashboard helps management move beyond monthly scorecards. Instead of discovering problems after the fact, leaders can spot weak conversion, low deposit growth, or operational service breakdowns while there is still time to respond.

Commercial banking requires stronger visibility into pipeline quality, relationship performance, and account behavior.

A commercial banking dashboard often tracks:

This helps commercial heads answer practical questions: Which pipelines are stalling? Which portfolios are underpenetrated? Which client relationships show cross-sell opportunity or elevated risk?

Risk and treasury teams need dashboards that combine speed, control, and governance readiness.

Typical use cases include:

These dashboards are especially useful when threshold logic and automated alerts are configured correctly. The objective is not only visibility, but fast escalation when indicators move beyond tolerance.

Digital leaders need a dashboard that connects usage data to customer behavior and business outcomes.

Common digital dashboard metrics include:

This is where a banking dashboard becomes a growth tool, not just a reporting tool. Digital journey visibility helps banks improve onboarding, reduce friction, and increase product uptake across self-service channels.

A useful banking dashboard starts with decision design, not chart design. Too many teams begin by asking what data is available. The better question is: What decision must this dashboard improve?

Define the high-value management questions first. For example:

When you start here, your dashboard stays focused on action rather than reporting noise.

Executives, managers, analysts, and frontline teams do not need the same view.

A strong design principle is:

This role alignment prevents overcomplication and improves adoption.

Banking dashboards should help users move from signal to diagnosis fast. The most effective layouts usually include:

Hierarchy matters. Users should immediately see what changed, where it changed, and what to investigate next.

A banking dashboard must feel usable under pressure. If users cannot interpret it in a few seconds, they will default back to spreadsheets and email.

Practical design rules include:

If you are building or redesigning a banking dashboard, these are the consultant-level steps that usually make the difference between adoption and abandonment.

Agree on calculation logic, ownership, refresh frequency, and exception thresholds. A dashboard fails quickly when finance, operations, and risk teams each define the same metric differently.

Design the dashboard according to how decisions are made. For example, a delinquency dashboard may need credit, collections, and branch inputs in one workflow, not three isolated views.

In banking, trust is everything. If users see stale balances, unexplained discrepancies, or broken drill-down logic, confidence drops immediately. Set clear refresh rules and visible data timestamps.

The best banking dashboard does not only show performance. It highlights where action is required. Add thresholds, alerting, red-amber-green logic, and owner-based escalation paths.

Do not launch an enterprise-wide dashboard framework all at once. Start with a high-impact scenario such as branch performance, loan turnaround, or liquidity monitoring. Prove value, refine adoption, then scale.

When reviewing banking dashboard examples, templates, or vendors, institutions should avoid being impressed by visual polish alone. A banking dashboard must support governance, decision quality, and operational scale.

Whether you are evaluating Power BI showcases, business banking resource hubs, financial dashboard template libraries, BCBS dashboards, or bank performance tools, review them against these criteria:

Use this shortlist before selecting a dashboard model or platform:

The methodology is clear: define business questions, standardize KPIs, design for role-based decisions, and build dashboards that move users from summary to root cause. But building this manually is complex.

Banks typically face the same implementation friction:

This is where FineBI becomes the practical solution.

Building this manually is complex; use FineBI to utilize ready-made templates and automate this entire workflow. FineBI helps banks accelerate dashboard delivery with faster data integration, reusable dashboard logic, role-based analytics, and scalable self-service reporting. Instead of starting from scratch every time, teams can use templates and standardized components to create banking dashboards for branch performance, risk oversight, customer analytics, operational efficiency, and executive reporting.

For enterprise decision-makers, the advantage is not just speed. It is control with flexibility:

If your institution wants a banking dashboard that supports strategic oversight, tactical management, and operational execution, FineBI offers a more efficient path than building and maintaining everything by hand. In practice, that means less time assembling data, more time acting on it, and better decisions across every layer of the bank.

A banking dashboard is used to bring key financial, customer, risk, compliance, and operational data into one interactive view. It helps bank leaders monitor performance, spot issues early, and make faster decisions.

A useful banking dashboard should focus on KPIs tied to action, such as revenue growth, net interest margin, cost-to-income ratio, deposit and loan growth, delinquency trends, digital adoption, and customer retention. The exact mix should match the user’s role and business goals.

Traditional reports are usually static and backward-looking, while a banking dashboard is interactive and designed for ongoing decisions. It typically supports drill-down analysis, filtering, alerts, and near-real-time visibility.

Banking dashboards are useful for executives, branch managers, operations teams, analysts, and risk or compliance leaders. Each group can use a role-based view to track the metrics most relevant to their responsibilities.

An effective banking dashboard has clear KPI definitions, reliable data sources, role-based design, and easy drill-down from summary to detail. It should help users act quickly rather than overwhelm them with too many charts.

The Author

Yida YIn

FanRuan Industry Solutions Expert

Related Articles

Dashboard Image Best Practices: 7 Ways to Clarify KPIs in Executive Reports

A dashboard image is only valuable if it helps an executive understand performance fast enough to make a decision. In leadership reporting, that is the standard. CFOs, COOs, business unit heads, and operations directors

Eric

Jan 01, 1970

Profitability Dashboard Examples, Templates, and KPIs: How to Build One That Drives Decisions

A profitability dashboard is not a reporting accessory. It is a decision system. For founders, CFOs, finance managers, and department heads, its job is simple: show where profit is created, where it leaks, and what actio

Eric

Jan 01, 1970

Why Most Dashboard LMS Setups Fail—and How to Build One That Improves Decisions

A dashboard lms is supposed to help training leaders, LMS administrators, instructors, and people managers make faster, better decisions. In practice, most dashboards do the opposite: they create noise, bury priorities,

Eric

Jan 01, 1970